Securing your financial future is a crucial step in achieving long-term peace of mind. As you navigate the complex world of investing, it’s essential to understand the diverse options available and select strategies that align with your financial goals and risk tolerance. While the concept of investing can seem intimidating, it’s a powerful tool that can help you build wealth and achieve financial independence. This article will delve into the realm of long-term investments, exploring some of the best options to secure your financial future.

From the safety of bonds to the potential for growth in the stock market, there are various investment avenues to consider. We’ll guide you through the intricacies of each option, discussing their unique advantages and disadvantages. We’ll also emphasize the importance of diversification and strategic asset allocation to mitigate risk and maximize returns. Whether you’re a seasoned investor or just starting your journey, this comprehensive guide will provide valuable insights and empower you to make informed decisions that pave the way towards a secure and prosperous future.

Defining Long-Term Investment Goals

Before diving into the world of long-term investments, it’s crucial to establish clear and well-defined goals. These goals will serve as your compass, guiding your investment decisions and keeping you motivated throughout the journey.

To begin, ask yourself: What are your financial aspirations? Are you aiming to retire comfortably, purchase a dream home, fund your children’s education, or achieve another specific milestone?

Next, consider the time horizon for your goals. Long-term investments typically involve a time frame of 5 years or more. Be realistic about the timeframe you’re working with, as it will influence your risk tolerance and investment strategy.

Lastly, quantify your goals. How much money do you need to achieve them? Having a concrete financial target in mind will provide a clear path to follow and help you track your progress.

By defining your long-term investment goals, you establish a strong foundation for making informed investment decisions and ultimately securing your financial future.

The Power of Compounding Returns

Compounding, often referred to as the “eighth wonder of the world,” is the magic of earning returns on your initial investment as well as on the accumulated earnings. This snowball effect allows your investments to grow exponentially over time, especially when coupled with long-term horizons.

Imagine investing a modest sum of $10,000 at a consistent 8% annual return. In just 20 years, your investment will have grown to over $46,600, solely through the power of compounding. This highlights the importance of patience and consistency when it comes to long-term investing.

To maximize the benefits of compounding, consider these factors:

- Start early: The earlier you begin investing, the longer your money has to compound and grow.

- Invest regularly: Consistent contributions, even small amounts, will significantly boost your returns over time.

- Choose high-yielding investments: Opt for investments that have the potential to deliver consistent, long-term returns.

- Stay invested: Avoid withdrawing your investments prematurely, as this interrupts the compounding process.

Understanding and harnessing the power of compounding is crucial for securing a strong financial future. By starting early, investing consistently, and choosing wise investments, you can leverage the magic of compounding to achieve your financial goals.

Exploring Different Asset Classes

When it comes to securing your financial future, understanding the various asset classes available is crucial. Asset classes are broad categories of investments with similar characteristics, risks, and returns. Diversifying your portfolio across different asset classes can help you mitigate risk and achieve your long-term financial goals.

Here are some of the most common asset classes:

Stocks (Equities)

Stocks represent ownership in a company. They tend to offer higher potential returns but also carry greater risk. Growth stocks focus on expanding businesses, while value stocks are companies trading at lower valuations. Large-cap stocks are issued by large companies, while small-cap stocks are issued by smaller companies.

Bonds

Bonds represent loans you make to governments or corporations. They typically offer lower returns than stocks but are considered less risky. Government bonds are issued by governments, while corporate bonds are issued by companies.

Real Estate

Real estate encompasses physical properties such as homes, apartments, and commercial buildings. It can offer diversification and potential appreciation, but it also comes with high costs and liquidity risks.

Commodities

Commodities are raw materials such as oil, gold, and agricultural products. They can serve as an inflation hedge and offer diversification. Gold is often considered a safe-haven asset during economic uncertainty.

Cash and Equivalents

Cash and equivalents include savings accounts, money market funds, and short-term government securities. While they offer low returns, they provide liquidity and safety.

Choosing the right asset allocation mix for your portfolio depends on your investment goals, risk tolerance, and time horizon. Consulting with a financial advisor can help you develop a tailored strategy that aligns with your individual needs and circumstances.

Real Estate: A Stable Investment

Real estate has long been considered a cornerstone of a diversified investment portfolio, offering a unique combination of stability, potential for appreciation, and income generation. Unlike stocks, bonds, or commodities, which can fluctuate wildly in value, real estate provides a tangible asset with intrinsic worth.

One of the primary advantages of investing in real estate is its inherent stability. While market fluctuations can impact property values, the underlying demand for housing remains a constant. As populations grow and economies thrive, the need for residential and commercial spaces continues to rise, making real estate a relatively secure investment. Moreover, unlike stocks, which can lose value overnight, real estate typically depreciates at a much slower pace, providing a more stable and predictable return on investment.

Another compelling reason to consider real estate is its potential for appreciation. Over time, property values tend to increase, especially in desirable locations with strong economic growth. This appreciation can generate significant returns, allowing investors to build wealth and achieve their financial goals. Factors like rising demand, limited supply, and economic prosperity can contribute to this upward trend in property values, making real estate a powerful tool for wealth creation.

Beyond potential appreciation, real estate offers the opportunity for income generation through rental properties. By investing in rental units or commercial spaces, investors can generate passive income streams, providing a steady flow of cash flow. This recurring revenue can be used to cover expenses, build equity, or supplement other income sources, enhancing financial security and stability.

In conclusion, real estate provides a robust investment option for individuals seeking a stable, appreciating, and income-generating asset. Its inherent stability, potential for appreciation, and income generation capabilities make it a valuable addition to any well-rounded investment portfolio, contributing to financial security and long-term wealth creation.

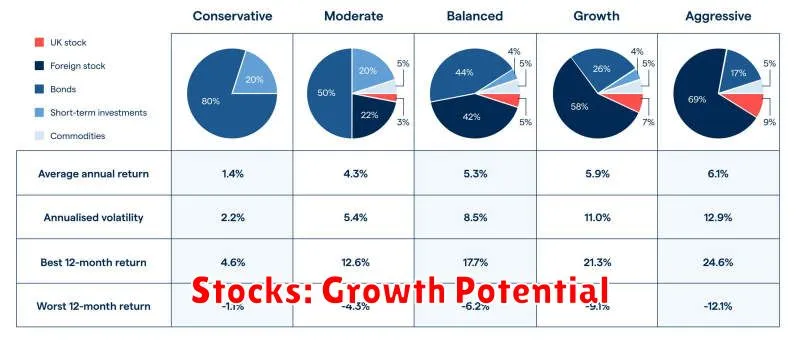

Stocks: Growth Potential

Stocks, also known as equities, represent ownership in a company. They offer the potential for significant growth over the long term, making them a popular choice for investors seeking to build wealth. When a company performs well and its profits increase, the value of its stock typically rises, allowing investors to profit from their investment. This growth potential is often attributed to several factors, including:

1. Business Expansion and Innovation: Companies that are constantly innovating, expanding their operations, and entering new markets often see their stock prices appreciate. This growth is driven by the potential for increased revenue and profitability.

2. Industry Trends: Companies operating in industries experiencing strong growth, such as technology, healthcare, or renewable energy, can benefit from increasing demand and market share. This can translate into higher stock prices.

3. Dividend Payments: Some companies distribute a portion of their profits to shareholders in the form of dividends. These regular payments can provide a consistent source of income and enhance the overall return on investment.

4. Market Sentiment: Investor confidence and market conditions play a crucial role in stock prices. When the market is optimistic, stock prices tend to rise. Conversely, negative sentiment can lead to price declines.

While stocks offer the potential for significant growth, it’s important to remember that they also carry inherent risks. Stock prices can fluctuate significantly, and investors may experience losses in the short term. However, over the long term, stocks have historically outperformed other asset classes, making them a valuable component of a diversified investment portfolio.

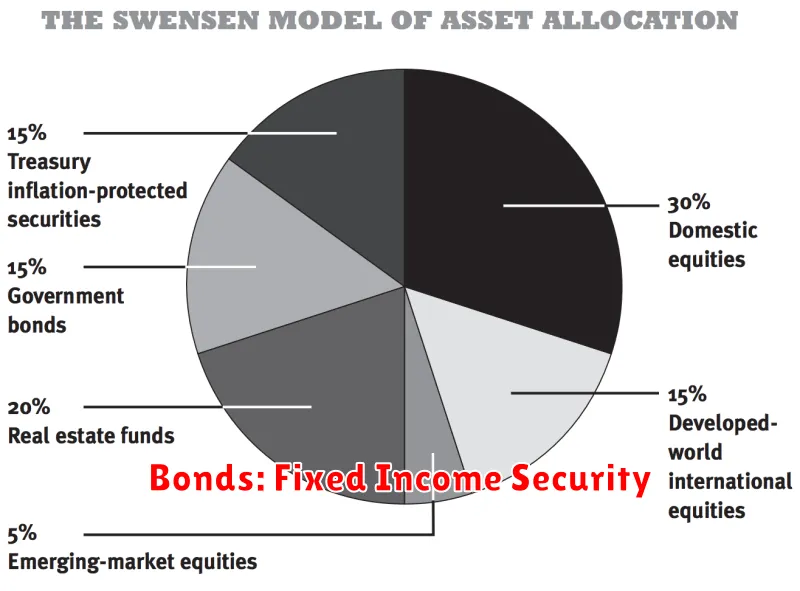

Bonds: Fixed Income Security

In the realm of long-term investments, bonds stand as a cornerstone, offering a steady stream of income and a measure of stability to your portfolio. Unlike stocks, which represent ownership in a company, bonds represent a loan that you provide to a borrower, typically a government or corporation. In exchange for this loan, the borrower promises to repay the principal amount at maturity, along with regular interest payments, known as coupon payments.

Bonds are often lauded for their predictable nature. As long as the borrower remains financially sound, you can count on receiving those coupon payments at predetermined intervals. Moreover, when the bond matures, you’ll get your principal back. This makes bonds a valuable addition to any diversified investment strategy.

However, it’s essential to understand that bond investments aren’t entirely risk-free. Interest rates fluctuate, and if they rise, the value of your existing bonds might fall. This is because investors will demand higher returns for newly issued bonds, making your older bonds with lower interest rates less attractive. Conversely, if interest rates decline, the value of your bonds could rise.

Despite the potential for volatility, bonds serve a crucial role in safeguarding your financial future. They provide a balanced counterpoint to the inherent risks associated with stocks. This balance can help you navigate market fluctuations and achieve your long-term financial goals.

When considering bonds, you’ll want to understand key characteristics like maturity date, coupon rate, and credit rating. Maturity date specifies when the principal will be repaid, the coupon rate determines the interest payments, and the credit rating indicates the borrower’s creditworthiness. By carefully evaluating these factors, you can select bonds that align with your investment goals and risk tolerance.

Mutual Funds and ETFs: Diversification Benefits

When it comes to investing for the long term, diversification is crucial. It helps mitigate risk and potentially boost returns. Two popular investment vehicles that offer excellent diversification benefits are mutual funds and exchange-traded funds (ETFs).

Mutual funds pool money from multiple investors to purchase a basket of securities, such as stocks, bonds, or real estate. By investing in a mutual fund, you gain exposure to a wide range of assets, effectively diversifying your portfolio across different sectors, industries, and asset classes.

ETFs, on the other hand, are similar to mutual funds but are traded on stock exchanges like individual stocks. They offer similar diversification benefits, allowing you to invest in a broad range of assets with a single purchase. ETFs are often known for their lower expense ratios compared to some mutual funds.

The diversification benefits of mutual funds and ETFs are significant for long-term investors. They help reduce the impact of individual asset performance on your overall portfolio. If one asset class experiences a downturn, other assets in your portfolio may perform well, cushioning the impact of the loss.

Furthermore, both mutual funds and ETFs are managed by professional portfolio managers, who actively select and manage the underlying assets. This expertise can provide investors with valuable insights and strategic decision-making, enhancing diversification and potentially improving returns.

In conclusion, mutual funds and ETFs offer invaluable diversification benefits for long-term investors. By spreading your investments across a range of assets, you can mitigate risk, potentially enhance returns, and build a more robust and resilient portfolio for your financial future.

Alternative Investments: Exploring New Avenues

When it comes to securing your financial future, traditional investments like stocks and bonds have long been the go-to options. However, in today’s volatile market, diversification is crucial. Alternative investments offer an intriguing avenue to explore, presenting unique opportunities to enhance portfolio returns and mitigate risks. Let’s delve into the world of alternative investments and uncover why they might be a valuable addition to your long-term investment strategy.

Alternative investments encompass a diverse range of asset classes beyond the conventional. These include:

- Real estate: From residential properties to commercial real estate, this asset class provides potential for rental income, appreciation, and tax benefits.

- Private equity: Investing in privately held companies, offering opportunities for significant growth but also higher risk.

- Hedge funds: Utilizing complex strategies and sophisticated investment techniques to generate returns in various market conditions.

- Commodities: Raw materials such as gold, oil, and agricultural products, offering inflation protection and potential diversification benefits.

- Digital assets: Including cryptocurrencies and NFTs, representing a burgeoning and potentially lucrative market with inherent volatility.

The allure of alternative investments lies in their potential to generate higher returns and offer diversification benefits. Real estate can provide stable rental income and potential appreciation, while private equity offers exposure to promising businesses that may not be accessible through public markets. Hedge funds can employ sophisticated strategies to capitalize on market inefficiencies and generate returns regardless of market direction. Commodities act as a hedge against inflation and can provide portfolio diversification. Finally, digital assets represent a rapidly evolving market with the potential for significant growth, albeit with heightened risk.

However, it’s crucial to approach alternative investments with caution. They often come with higher risk profiles, illiquidity, and potential for complexity. Understanding the intricacies of each asset class, conducting thorough research, and seeking professional advice are essential steps before embarking on this investment journey.

By diversifying your portfolio with a carefully selected mix of alternative investments, you can potentially enhance returns, mitigate risk, and create a more robust foundation for your long-term financial security.

Factors to Consider Before Investing

Investing is a crucial step towards securing your financial future, but it’s essential to approach it strategically. Before diving into any investment, it’s vital to consider several key factors that will influence your success. These factors encompass your personal circumstances, risk tolerance, financial goals, and the investment itself.

1. Your Financial Goals and Time Horizon

Clearly defining your financial goals is paramount. Are you saving for retirement, a down payment on a house, or your children’s education? Once you know your goals, determine a realistic time horizon for achieving them. This will help you select appropriate investments that align with your timeline.

2. Risk Tolerance

Everyone has a different level of risk tolerance. Some individuals are comfortable with potentially high returns, while others prioritize preserving capital. Assess your risk tolerance honestly. If you’re risk-averse, you might prefer investments like bonds or real estate. Conversely, if you’re willing to take on more risk, stocks or other growth-oriented investments could be suitable.

3. Investment Knowledge and Experience

It’s essential to understand the investment options available and their associated risks and rewards. If you’re a novice investor, starting with a diversified portfolio of low-risk investments like index funds or ETFs can be a wise choice. As your knowledge and experience grow, you can gradually explore more complex investment strategies.

4. Market Conditions

The market conditions can significantly impact investment returns. It’s crucial to stay informed about current economic trends, interest rates, and market volatility. While you can’t control the market, understanding its dynamics can help you make informed investment decisions.

5. Fees and Expenses

Don’t overlook the fees and expenses associated with investing. These can significantly impact your returns over time. Compare different investment options and choose those with reasonable fees and transparent expense structures.

6. Diversification

Diversification is a fundamental principle of investing. By spreading your investments across different asset classes, sectors, and geographies, you reduce your overall risk. A diversified portfolio can help cushion the impact of potential losses in one particular area.

By carefully considering these factors, you can make informed investment decisions that align with your financial goals and risk tolerance. Remember, investing is a journey, and it’s crucial to be patient, disciplined, and adaptable throughout the process.

Managing Risk in Long-Term Investments

Investing for the long term is essential for building a secure financial future. However, it’s crucial to acknowledge and manage the inherent risks associated with any investment. Long-term investments offer the potential for significant returns, but they also come with the possibility of market fluctuations and unexpected events. Here’s how to navigate the complexities of risk management in long-term investing:

Diversification: Spreading your investments across different asset classes, such as stocks, bonds, real estate, and commodities, reduces the impact of any single investment’s performance on your overall portfolio. Diversification helps mitigate risk by creating a balanced and resilient portfolio.

Time Horizon: The longer your investment horizon, the more time you have to recover from market downturns. Long-term investments allow you to ride out short-term volatility and benefit from the long-term growth potential of the market. Patience and a disciplined approach are key to success.

Risk Tolerance: Understanding your own risk tolerance is essential. This involves assessing your comfort level with potential losses and your willingness to accept volatility. If you’re risk-averse, you might prioritize low-risk investments, while those with higher risk tolerance may be comfortable with investments that have the potential for greater returns but also higher volatility.

Professional Advice: Seeking guidance from a qualified financial advisor can be invaluable. They can help you develop an investment strategy that aligns with your financial goals, risk tolerance, and time horizon. A financial advisor can also provide ongoing monitoring and adjustments to your portfolio to help you stay on track.

Regular Monitoring: Regularly review your investments to ensure they remain aligned with your financial goals and risk tolerance. Be prepared to adjust your investment strategy as your circumstances and market conditions change. This proactive approach can help you stay ahead of potential risks and maximize your returns.

Building a Diversified Long-Term Portfolio

A well-diversified long-term portfolio is a cornerstone of securing your financial future. It’s about strategically allocating your investments across different asset classes to manage risk and optimize returns. By spreading your investments, you mitigate the impact of any single asset’s poor performance, enhancing the overall stability and growth potential of your portfolio.

Here’s a breakdown of key asset classes to consider:

- Stocks: Represent ownership in companies. They offer potential for high returns but carry more volatility than bonds.

- Bonds: Represent loans to governments or companies, providing a more stable income stream than stocks.

- Real Estate: Offers potential for capital appreciation and rental income, but involves higher liquidity risks.

- Commodities: Raw materials like gold, oil, and agricultural products. They can act as a hedge against inflation but also exhibit price volatility.

- Cash: Serves as a safe haven during market downturns, but offers limited growth potential.

The optimal allocation depends on your individual circumstances, including your risk tolerance, investment goals, and time horizon. It’s crucial to seek professional financial advice to determine the right mix for you. Regularly rebalancing your portfolio ensures you maintain your desired asset allocation over time.

Building a diversified long-term portfolio is an ongoing process, requiring patience and discipline. By thoughtfully choosing assets, managing risk, and consistently rebalancing, you can create a resilient portfolio that can help you achieve your financial goals and secure a brighter future.

Reviewing and Rebalancing Your Portfolio

A well-structured investment portfolio is a cornerstone of financial security. It’s not a “set it and forget it” endeavor, though. As your life evolves, your investment goals and risk tolerance may shift. That’s why it’s crucial to regularly review and rebalance your portfolio.

Reviewing your portfolio involves analyzing its performance, evaluating your current asset allocation, and examining your overall investment strategy. This process allows you to identify any areas that need adjustments. Rebalancing, on the other hand, is the act of adjusting your portfolio’s asset allocation back to your original target percentages. This helps maintain your desired risk level and ensures you’re not overexposed to any specific asset class.

Here are some key factors to consider when reviewing and rebalancing your portfolio:

- Time horizon: Your investment time horizon is the length of time you plan to hold your investments. As you get closer to your financial goals, you may want to shift towards a more conservative investment approach.

- Risk tolerance: Your risk tolerance is your ability and willingness to accept potential losses in exchange for the possibility of higher returns. As your life circumstances change, your risk tolerance may also change.

- Market conditions: Market conditions are constantly changing. What was a good investment strategy a few years ago may no longer be appropriate today. It’s important to stay updated on market trends and adjust your portfolio accordingly.

- Financial goals: Your financial goals may change over time, such as purchasing a home, funding your child’s education, or retiring early. Your portfolio should be aligned with your evolving goals.

Regularly reviewing and rebalancing your portfolio can help you stay on track to achieve your financial goals. By taking the time to assess your investments and make adjustments as needed, you can enhance your chances of long-term success.

{kind=link}