Are you ready to secure your financial future and enjoy a comfortable retirement? Planning for retirement can seem daunting, but with the right strategies and investments, you can build a solid foundation for a fulfilling life after work. This comprehensive guide will delve into the best investment options available, equipping you with the knowledge and tools to make informed decisions and reach your retirement goals.

From stocks and bonds to real estate and retirement accounts, we’ll explore the diverse landscape of investment opportunities. We’ll analyze the pros and cons of each option, considering factors like risk tolerance, time horizon, and individual financial circumstances. You’ll gain insights into the most effective ways to diversify your portfolio, manage risk, and maximize returns. Let’s embark on this journey together and build a future where you can retire with confidence and financial freedom.

Understanding Your Retirement Goals and Risk Tolerance

Retirement planning is a marathon, not a sprint. It requires a deep understanding of your financial goals and risk tolerance. This crucial step sets the foundation for your investment strategy and helps you navigate the complex world of retirement savings.

Defining Your Retirement Goals

Start by asking yourself: What kind of retirement do you envision? Do you dream of traveling the world, pursuing hobbies, or simply enjoying a comfortable lifestyle? Clarify your desired retirement lifestyle and quantify your financial needs. This could involve factors like your desired income level, housing expenses, healthcare costs, and any other personal aspirations.

Assessing Your Risk Tolerance

Risk tolerance refers to your ability and willingness to accept potential losses in exchange for the possibility of higher returns. Consider your comfort level with market fluctuations. A younger investor with a longer time horizon might be more comfortable taking on higher risks. Conversely, someone closer to retirement may prefer a more conservative approach to protect their savings.

Matching Your Goals and Risk Tolerance

Once you have a clear understanding of your retirement goals and risk tolerance, you can start building an investment portfolio that aligns with both. A financial advisor can help you navigate this process, providing personalized guidance and recommendations based on your unique circumstances. Remember, the key to successful retirement planning is to create a strategy that is both realistic and sustainable over the long term.

Traditional Retirement Savings Plans: 401(k)s and IRAs

Traditional retirement savings plans, such as 401(k)s and IRAs, are powerful tools for building a secure financial future. These plans offer tax advantages and potential growth opportunities, making them essential components of any retirement savings strategy. Let’s delve into the intricacies of these plans to understand their benefits and how they can help you achieve your retirement goals.

401(k)s: Employer-Sponsored Plans

A 401(k) is a retirement savings plan offered by employers. Employees can contribute a portion of their pre-tax income to the plan, and their contributions are often matched by the employer. This matching feature is a significant perk, essentially providing free money towards retirement savings. 401(k)s offer tax deferral, meaning you won’t pay taxes on your contributions or earnings until you withdraw them in retirement.

IRAs: Individual Retirement Accounts

An IRA is a retirement savings plan that individuals can open independently. Unlike 401(k)s, IRAs are not employer-sponsored. There are two primary types of IRAs: traditional and Roth. Traditional IRAs offer tax-deductible contributions, reducing your taxable income in the present. Roth IRAs, on the other hand, involve after-tax contributions but provide tax-free withdrawals in retirement. Choosing between a traditional and Roth IRA depends on your individual financial circumstances and tax projections.

Key Advantages of Traditional Retirement Savings Plans

Traditional retirement savings plans offer several advantages, including:

- Tax Benefits: Both 401(k)s and traditional IRAs provide tax deferral, allowing your contributions and earnings to grow tax-free until retirement.

- Potential for Growth: These plans allow your savings to grow over time through investments in stocks, bonds, and other assets.

- Employer Matching: 401(k)s often offer employer matching contributions, essentially giving you free money towards retirement.

Conclusion

Traditional retirement savings plans like 401(k)s and IRAs are indispensable tools for securing your financial future. By taking advantage of the tax benefits, growth potential, and employer matching offered by these plans, you can build a robust nest egg for a comfortable retirement.

The Power of Diversification: Spreading Your Retirement Investments

Diversification is a fundamental principle in investing, especially when it comes to retirement planning. It involves spreading your investments across different asset classes, such as stocks, bonds, real estate, and commodities. This strategy helps mitigate risk and enhance potential returns over the long term.

Imagine putting all your retirement eggs in one basket, let’s say just stocks. If the stock market takes a downturn, your entire nest egg could be significantly impacted. Diversification allows you to reduce this risk by spreading your investments across various asset classes. When one asset class performs poorly, another might perform well, balancing out the overall portfolio.

Here’s how diversification works in practice:

- Stocks: Equities offer the potential for higher returns but also carry higher risk. Diversifying within stocks involves investing in different sectors, company sizes, and geographical regions.

- Bonds: Bonds are generally considered less risky than stocks, providing steady income and stability to a portfolio. Diversification in bonds involves investing in different maturities, credit ratings, and types of bonds.

- Real Estate: Real estate can offer diversification benefits, especially in a portfolio with a significant stock allocation. It can provide rental income and potential appreciation.

- Commodities: Commodities such as gold and oil can serve as a hedge against inflation and provide diversification to a portfolio.

By diversifying your retirement investments, you can:

- Reduce risk: Spreading your investments across different asset classes mitigates the impact of any single asset class’s poor performance.

- Enhance potential returns: A diversified portfolio has the potential to generate higher returns over time by taking advantage of the upswings in different asset classes.

- Increase your peace of mind: Knowing your investments are well-diversified can give you greater confidence and peace of mind during market fluctuations.

Remember: Diversification is not a guarantee against losses. It is a risk management strategy that can help minimize potential losses and enhance the overall performance of your portfolio over the long term.

Consult with a financial advisor to create a personalized diversification strategy that aligns with your risk tolerance, investment goals, and time horizon. By understanding the power of diversification and implementing it effectively, you can take a significant step towards securing your financial future and enjoying a comfortable retirement.

Exploring Different Asset Classes: Stocks, Bonds, and Real Estate

When it comes to securing your financial future, investing is key. But with countless options available, it can be daunting to know where to start. Understanding different asset classes and their potential benefits is crucial for making informed investment decisions. Three prominent asset classes that often form the core of investment portfolios are stocks, bonds, and real estate.

Stocks represent ownership in a company. By investing in stocks, you become a shareholder, potentially benefiting from company growth and dividends. Stocks are generally considered higher-risk investments, offering the potential for significant returns but also volatility. However, over the long term, stocks have historically outperformed other asset classes.

Bonds, on the other hand, represent loans you make to a company or government. When you buy a bond, you are lending money and receiving interest payments in return. Bonds are generally considered lower-risk than stocks, providing a more stable and predictable income stream. However, their potential returns are also typically lower.

Real estate encompasses properties such as homes, apartments, and commercial buildings. Investing in real estate can provide a stream of rental income, appreciation in value, and tax benefits. However, it also requires significant capital, can be illiquid, and involves ongoing expenses for maintenance and management.

The ideal asset allocation for your portfolio depends on your individual circumstances, risk tolerance, and investment goals. Consider consulting with a financial advisor to determine the right mix of assets for your unique needs.

Low-Risk Investments for Retirement: Preserving Capital

As you approach retirement, preserving your hard-earned capital becomes paramount. While seeking growth is important, safeguarding your principal against significant losses takes priority. Low-risk investments offer a balance between potential returns and minimizing downside risk, providing peace of mind during your golden years.

Here are some low-risk investments suitable for retirement planning:

1. High-Yield Savings Accounts (HYSA)

HYSAs offer higher interest rates than traditional savings accounts, providing a modest return while maintaining FDIC insurance. This option is ideal for emergency funds or short-term savings goals, offering liquidity and stability.

2. Certificates of Deposit (CDs)

CDs offer fixed interest rates for a specified period, ensuring a predictable return. While early withdrawal penalties exist, they provide a secure haven for funds you won’t need immediately. Choose CDs with maturities aligning with your retirement timeline.

3. U.S. Treasury Securities

U.S. Treasury securities are backed by the full faith and credit of the U.S. government, making them exceptionally safe. They offer a range of maturities, from short-term bills to long-term bonds, catering to diverse risk tolerances and investment horizons.

4. Money Market Funds

Money market funds invest in short-term, highly liquid debt instruments, offering stable returns with minimal risk. They provide easy access to your funds, making them suitable for emergency reserves or short-term goals.

5. Annuities

Annuities offer a guaranteed stream of income for life, providing financial security in retirement. They are ideal for those seeking predictable cash flow, though they can have complex terms and fees. Consult with a financial advisor before investing.

6. Dividend-Paying Stocks

While stocks carry inherent risk, dividend-paying stocks offer a steady stream of income. Choose companies with a strong track record of dividend payments and a solid financial foundation.

Remember, your retirement planning strategy should align with your individual needs, goals, and risk tolerance. Consulting with a financial advisor can help you create a diversified portfolio that balances growth potential and capital preservation.

Growth Investments for Retirement: Aiming for Higher Returns

As you plan for a comfortable retirement, it’s crucial to consider investments that can provide the potential for higher returns. Growth investments, characterized by their potential for significant appreciation over time, can play a vital role in reaching your financial goals. While these investments may come with greater risk, their potential for long-term growth can be substantial.

One popular category of growth investments is equities, which represent ownership in companies. Stocks, particularly those of companies with strong growth potential, can deliver significant returns over the long term. However, it’s essential to remember that stock prices can fluctuate significantly, and investors should have a long-term perspective when considering equities.

Another option is real estate, which can provide both income and appreciation potential. Investing in rental properties or commercial real estate can generate cash flow and potentially increase in value over time. However, real estate investments require significant capital and involve ongoing management responsibilities.

Alternative investments, such as venture capital, private equity, and hedge funds, offer unique opportunities for growth but often come with higher risk and limited liquidity. These investments are typically suitable for experienced investors with a high risk tolerance and long investment horizon.

When considering growth investments for retirement, it’s essential to remember that diversification is key. By spreading your investments across different asset classes, you can mitigate risk and potentially enhance returns. It’s also crucial to consult with a financial advisor who can help you develop a personalized investment strategy that aligns with your risk tolerance, time horizon, and retirement goals.

The Role of Social Security in Retirement Planning

Social Security is a vital component of retirement planning, offering a steady stream of income that can help cover essential expenses. While it’s not designed to be your sole source of retirement income, it plays a crucial role in supplementing other savings and investments. Understanding how Social Security works and how it integrates with your overall retirement plan is essential for a secure future.

Benefits of Social Security:

- Guaranteed Income: Social Security provides a reliable source of income that is not subject to market fluctuations.

- Inflation Adjustments: Benefits are adjusted annually to keep pace with inflation, ensuring their purchasing power remains stable.

- Lifelong Coverage: Benefits can continue for life, providing ongoing support throughout retirement.

Maximizing Your Social Security Benefits:

- Delayed Retirement: Claiming benefits after your full retirement age (FRA) results in higher monthly payments. Consider delaying retirement to maximize your benefits.

- Working While Receiving Benefits: You can continue working while receiving Social Security benefits. Your benefits may be adjusted based on your earnings, but this can be beneficial for increasing your overall retirement income.

- Understanding Earnings Limitations: Be aware of the earnings limitations for claiming Social Security benefits before your FRA. Exceeding these limits can reduce your benefits.

Integrating Social Security into Your Retirement Plan:

- Estimate Your Benefits: Use the Social Security Administration’s website to estimate your future benefits based on your earnings history.

- Factor Benefits into Your Planning: Incorporate your estimated Social Security benefits into your overall retirement income projections.

- Diversify Your Retirement Income Sources: Don’t rely solely on Social Security. Diversify your income sources with savings, investments, and potentially part-time work.

Social Security is an essential part of retirement planning, offering a guaranteed source of income and providing a foundation for financial security. By understanding how it works and incorporating it into your overall plan, you can maximize its benefits and build a solid foundation for a comfortable retirement.

Retirement Planning Considerations at Different Life Stages

Retirement planning is a lifelong journey that requires careful consideration at every stage of life. Your financial goals and priorities will shift as you age, and your investment strategy should adapt accordingly. Here’s a breakdown of key retirement planning considerations at different life stages:

Early Career (20s-30s)

This is the time to build a strong financial foundation. Focus on:

- Saving early and often: Start contributing to a 401(k) or IRA as soon as possible, even if it’s a small amount. The magic of compounding will work its wonders over time.

- Minimizing debt: Prioritize paying down high-interest debt like credit cards. This frees up more cash flow for saving.

- Diversifying investments: Explore a mix of stocks, bonds, and other asset classes for potential growth and risk management.

Mid-Career (40s-50s)

Your career is established, and your family responsibilities may be peaking.

- Increase savings contributions: Boost your contributions to retirement accounts to maximize tax advantages and build a substantial nest egg.

- Rebalance your portfolio: As you approach retirement, consider shifting your portfolio towards more conservative investments to protect your principal.

- Plan for major expenses: Factor in potential costs like college tuition for children, home renovations, or healthcare.

Pre-Retirement (50s-60s)

The countdown to retirement begins!

- Review your retirement goals: Determine how much income you’ll need and adjust your savings plan accordingly.

- Consider withdrawal strategies: Research different retirement income streams, such as Social Security, pensions, and withdrawals from retirement accounts.

- Minimize taxes: Utilize tax-efficient strategies to preserve your retirement savings.

Retirement (65+)

Congratulations! It’s time to enjoy the fruits of your labor.

- Manage your retirement funds: Draw down your savings strategically to ensure a sustainable income stream.

- Stay informed about healthcare: Prepare for potential healthcare costs and explore Medicare options.

- Consider estate planning: Update your will and estate plans to protect your loved ones.

Remember, retirement planning is an ongoing process. Regularly review your financial goals, make adjustments as needed, and consult with a financial advisor to ensure you’re on track to achieve a secure and comfortable retirement.

Managing Retirement Income: Strategies for Sustainability

Retirement is a significant life transition, and ensuring a comfortable and sustainable income stream is crucial for a fulfilling post-work life. As you approach retirement, it’s essential to develop a comprehensive strategy for managing your retirement income. This involves carefully considering your financial goals, risk tolerance, and lifestyle preferences.

One key strategy is to diversify your income sources. Reliance on a single source, like Social Security or a 401(k), can leave you vulnerable to unexpected changes or market fluctuations. Diversifying your income streams through investments, part-time work, or other sources can provide a buffer and enhance your financial security.

Another essential aspect is strategic withdrawal. Creating a plan for withdrawing funds from your retirement accounts is crucial to ensure you don’t outlive your savings. Consider a gradual withdrawal approach, taking into account factors like inflation, taxes, and potential longevity.

Furthermore, monitoring your expenses and adjusting your spending habits is vital for sustainability. As your income streams may shift in retirement, it’s essential to maintain a budget that aligns with your income and financial goals. This may involve reducing discretionary spending, exploring cost-effective alternatives, or finding ways to supplement your income.

Seeking professional financial advice can be invaluable in developing a sustainable retirement income plan. A financial advisor can help you assess your financial situation, create a personalized strategy, and provide ongoing guidance as you navigate the complexities of retirement planning.

In addition to these strategies, staying informed about changes in tax laws and retirement rules is crucial. Regulations and policies can evolve, potentially impacting your retirement income. Keeping abreast of these changes helps you adjust your plan and make informed decisions about your finances.

Managing your retirement income effectively requires a proactive approach and a commitment to financial responsibility. By implementing these strategies and seeking professional guidance, you can enhance your chances of achieving a comfortable and sustainable retirement.

Estate Planning Essentials: Protecting Your Legacy

As you navigate your financial journey, one of the most vital aspects to consider is estate planning. This crucial process ensures that your assets are distributed according to your wishes, safeguarding your legacy and providing for your loved ones after you’re gone. A robust estate plan acts as a roadmap, guiding the distribution of your assets, minimizing taxes, and preventing potential legal disputes. It encompasses a wide range of components, including a will, trusts, powers of attorney, and health care directives.

A will is a legally binding document that outlines how your assets will be distributed upon your death. It allows you to designate beneficiaries for your property, including real estate, bank accounts, and personal belongings. Trusts, on the other hand, provide a framework for managing assets and distributing them over time. They offer flexibility in asset allocation and can help minimize estate taxes.

Powers of attorney are crucial for granting someone the authority to make financial decisions on your behalf if you become incapacitated. Health care directives provide guidance for your medical care should you be unable to make decisions for yourself.

Estate planning is an essential aspect of ensuring your financial future. By taking the time to create a comprehensive plan, you can protect your legacy, provide for your loved ones, and secure peace of mind knowing that your assets will be managed according to your wishes.

Seeking Professional Financial Advice for Retirement Planning

Retirement planning is a crucial aspect of securing your financial future. It requires careful consideration of various factors such as your savings goals, investment strategies, and risk tolerance. While you can certainly research and manage your retirement planning on your own, seeking professional financial advice can provide significant benefits and help you make informed decisions.

A qualified financial advisor can offer personalized guidance tailored to your specific circumstances. They will assess your financial situation, understand your retirement objectives, and recommend suitable investment strategies. Financial advisors can help you develop a comprehensive retirement plan, diversify your portfolio, and manage your assets effectively.

Here are some key reasons why seeking professional financial advice is beneficial for your retirement planning:

- Objectivity: Financial advisors provide an unbiased perspective, helping you avoid emotional decisions that could jeopardize your retirement goals.

- Expertise: They possess specialized knowledge of financial markets, investment products, and retirement planning strategies.

- Personalized Solutions: They tailor their advice to your individual needs, considering your age, income, expenses, and risk tolerance.

- Ongoing Support: Financial advisors provide ongoing support and guidance throughout your retirement journey, adjusting your plan as needed.

When seeking financial advice, it is essential to choose a reputable and qualified advisor. Look for someone who is registered with the appropriate regulatory bodies, has a proven track record, and aligns with your values and investment philosophy.

In conclusion, seeking professional financial advice is an essential step in ensuring a comfortable and secure retirement. A qualified financial advisor can provide valuable insights, guidance, and support to help you achieve your retirement goals and enjoy your golden years with peace of mind.

Common Retirement Planning Mistakes to Avoid

Retirement planning is crucial for securing a comfortable financial future, but many individuals make common mistakes that can derail their savings goals. Avoiding these pitfalls can significantly enhance your chances of achieving a fulfilling retirement.

1. Procrastination: One of the biggest mistakes is delaying retirement planning. Time is your greatest asset, and the earlier you start saving, the more time your money has to grow through compounding. Don’t wait until the last minute to begin.

2. Underestimating Costs: Many people underestimate the expenses associated with retirement. Healthcare, travel, and leisure activities can significantly impact your budget. Create a realistic budget that considers all potential expenses.

3. Not Adjusting for Inflation: Inflation erodes the purchasing power of your savings over time. It’s important to factor in inflation when calculating your retirement needs. Consider investing in assets that tend to outpace inflation.

4. Overreliance on Social Security: Social Security is meant to supplement retirement income, not be the sole source. Don’t rely on it as your primary income stream.

5. Lack of Diversification: Putting all your eggs in one basket can be risky. Diversify your investments across different asset classes, such as stocks, bonds, and real estate, to mitigate risk.

6. Taking on Too Much Debt: High debt levels can hinder your retirement savings. Aim to pay down debt, especially high-interest loans, before retirement.

7. Ignoring Healthcare Costs: Healthcare expenses can escalate in retirement. Consider purchasing supplemental health insurance or saving specifically for healthcare costs.

8. Failing to Review Regularly: Your financial situation and goals can change over time. Regularly review your retirement plan and make adjustments as needed.

By avoiding these common mistakes, you can increase your chances of achieving a comfortable and secure retirement. Seek professional financial advice if needed to develop a personalized plan that aligns with your individual circumstances.

Best Retirement Investments for Early Retirement

Early retirement is a dream for many, but it requires careful planning and a solid financial foundation. One of the most crucial aspects of this journey is choosing the right investments to secure your financial future. With a diverse portfolio tailored for early retirement, you can enjoy the freedom and flexibility of retiring early without compromising your long-term financial well-being.

Here are some of the best retirement investments for those seeking an early exit from the traditional work schedule:

1. High-Yield Savings Accounts (HYSA)

HYSAs offer a relatively safe and accessible way to grow your savings while earning a competitive interest rate. They provide liquidity, allowing you to withdraw funds easily if needed. While the returns might not be as high as other investments, HYSAs can be a valuable component of your early retirement portfolio, especially during the initial accumulation phase.

2. Index Funds

Index funds are passively managed funds that track a specific market index, such as the S&P 500. They offer diversification and low expenses, making them an excellent choice for long-term growth. Index funds are a great way to invest in the overall market without needing to actively select individual stocks.

3. Real Estate

Real estate can be a powerful investment for early retirement, offering both income generation and potential appreciation. You can consider investing in rental properties, vacation rentals, or even your own primary residence. Real estate can provide a steady stream of passive income while building equity over time. However, it’s essential to conduct thorough research and consider the potential risks involved.

4. Dividend Stocks

Dividend stocks offer a combination of capital appreciation and regular income streams. By investing in companies that pay dividends, you can receive a steady flow of cash while also benefiting from potential stock price growth. Choose companies with a history of consistent dividend payments and strong financial performance.

5. Annuities

Annuities are insurance contracts that guarantee a stream of income payments for a specified period. While they can be complex, annuities can provide peace of mind in retirement by offering a predictable income stream. Consider consulting with a financial advisor to determine if an annuity is suitable for your specific circumstances.

Remember that investing for early retirement requires a long-term perspective. It’s crucial to diversify your portfolio, manage risk, and adjust your investments as your needs evolve. By carefully considering these investments and working with a financial advisor, you can create a strong financial foundation for a comfortable and fulfilling early retirement.

Tax-Efficient Retirement Investing: Minimizing Your Tax Burden

Retirement planning is crucial for ensuring financial security in your later years. A key aspect of this planning involves making tax-efficient investment choices. By minimizing your tax burden, you can maximize the growth of your retirement savings and enjoy a more comfortable retirement.

Tax-Advantaged Retirement Accounts:

Traditional and Roth IRAs, 401(k)s, and 403(b)s offer tax advantages. Traditional IRAs allow for pre-tax contributions, reducing your current tax liability, while withdrawals are taxed in retirement. Roth IRAs, on the other hand, involve after-tax contributions, but withdrawals in retirement are tax-free. 401(k)s and 403(b)s are employer-sponsored plans with similar tax benefits.

Tax-Loss Harvesting:

This strategy involves selling losing investments to offset capital gains, reducing your overall tax liability. You can use the proceeds from the sale to reinvest in similar assets, potentially reducing your tax burden.

Long-Term Capital Gains:

Holding investments for longer periods can lead to lower tax rates on capital gains. Long-term capital gains are typically taxed at lower rates than short-term gains. Investing in a diversified portfolio of stocks and bonds with a long-term horizon can be beneficial for tax efficiency.

Tax-Free Municipal Bonds:

These bonds are issued by state and local governments and offer interest income that is exempt from federal income tax. They can be a valuable addition to a retirement portfolio for investors seeking tax-free income.

Estate Planning:

Estate planning strategies like trusts and charitable donations can help minimize taxes on your retirement savings when passed on to heirs. Consult with a financial advisor and estate planning attorney to ensure your assets are distributed effectively and tax-efficiently.

Professional Advice:

Working with a qualified financial advisor specializing in retirement planning is essential for making informed decisions and developing a tax-efficient investment strategy. They can help you understand your tax situation, evaluate your investment options, and develop a personalized plan that meets your specific needs.

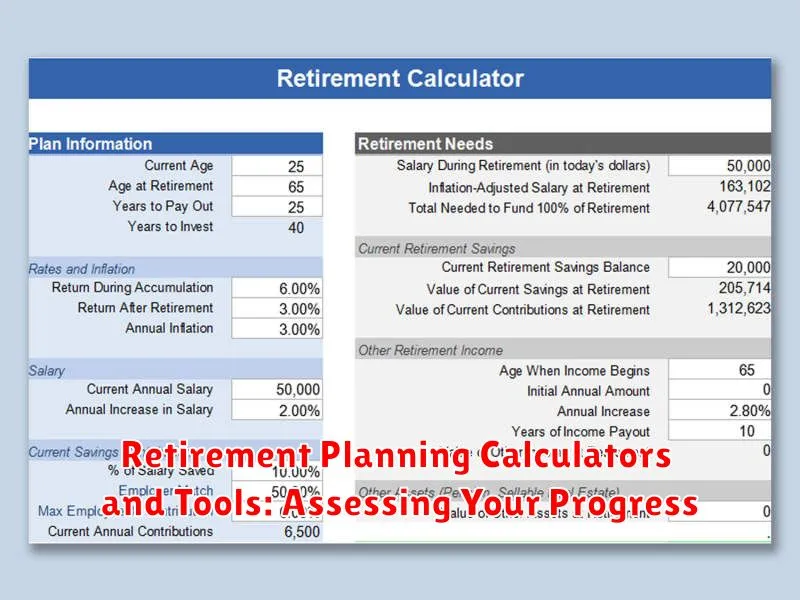

Retirement Planning Calculators and Tools: Assessing Your Progress

Retirement planning isn’t a one-time event; it’s an ongoing journey. To ensure you’re on track, utilizing retirement planning calculators and tools is essential. These handy resources provide valuable insights into your current savings, projected future needs, and potential outcomes. By inputting key information like your current age, desired retirement age, income, expenses, and expected investment returns, these tools can generate personalized estimates that help you visualize your financial future.

Retirement calculators offer a quick snapshot of your progress, while more sophisticated retirement planning tools delve deeper into your financial situation. These tools can assess your investment portfolio, suggest adjustments for optimal growth, and highlight potential areas of improvement. They also enable you to explore various “what-if” scenarios, allowing you to understand the impact of different savings habits and investment strategies.

Remember, these tools are only as accurate as the data you input. Ensure your information is up-to-date and realistic to get the most reliable estimates. Don’t be afraid to experiment with different scenarios and seek professional advice when needed. By leveraging these tools, you can gain a clearer picture of your retirement readiness and make informed decisions that secure your financial future.

{kind=link}