Renting a car can be a convenient and affordable way to get around, but it’s important to understand the ins and outs of car rental insurance. This comprehensive guide will cover everything you need to know about car rental insurance, including the different types of coverage, the costs involved, and how to make sure you’re adequately protected. We’ll also discuss common rental car insurance scams and how to avoid them, so you can relax and enjoy your trip without worrying about unexpected expenses.

Understanding Different Types of Car Insurance

Car insurance is a vital aspect of car ownership, providing financial protection in case of accidents, theft, or other unforeseen events. It’s essential to understand the different types of car insurance available to choose the right coverage for your needs and budget.

Liability Insurance

Liability insurance is a mandatory requirement in most states, covering damages you cause to other people or their property in an accident. It’s divided into two types:

- Bodily Injury Liability: Pays for medical expenses, lost wages, and other damages incurred by injured individuals in an accident.

- Property Damage Liability: Covers repairs or replacement costs for damaged property, such as vehicles or buildings.

Collision Coverage

Collision coverage protects your vehicle from damages resulting from a collision with another car or object. It pays for repairs or replacement costs, regardless of who’s at fault.

Comprehensive Coverage

Comprehensive coverage covers damages to your car caused by events other than collisions, such as theft, vandalism, fire, hail, or natural disasters. It also provides coverage for damages caused by animals or falling objects.

Uninsured/Underinsured Motorist Coverage

This coverage protects you if you’re involved in an accident with an uninsured or underinsured driver. It pays for your medical expenses and property damage, even if the other driver doesn’t have sufficient insurance.

Personal Injury Protection (PIP)

PIP coverage, also known as no-fault insurance, covers your medical expenses, lost wages, and other related costs, regardless of who’s at fault in an accident. This coverage is typically available in states with no-fault insurance laws.

Other Types of Car Insurance

Besides the basic types of car insurance, there are additional coverage options you can consider, such as:

- Gap Insurance: Covers the difference between your car’s value and the amount owed on your loan if your car is totaled.

- Rental Reimbursement: Pays for rental car expenses if your car is damaged or stolen and you need transportation.

- Roadside Assistance: Provides emergency services, such as towing, flat tire changes, and jump starts.

Choosing the Right Coverage

Determining the right type and amount of car insurance depends on several factors, including:

- Your driving history: A good driving record can lower your premiums.

- The value of your car: Newer or more expensive cars may require higher coverage amounts.

- Your financial situation: Consider your budget and the potential risks associated with driving.

It’s essential to consult with a reputable insurance agent to get personalized advice and find the most appropriate coverage for your needs. Remember, having adequate car insurance provides peace of mind and financial protection in case of unexpected events.

Why Rental Car Insurance Matters

When you rent a car, you’re essentially borrowing someone else’s vehicle. This means you’re responsible for any damage or accidents that occur while you’re driving it. This can be a lot of responsibility, and it’s important to understand the different types of insurance available to you when renting a car.

Rental car insurance is a type of insurance that covers you for damage or theft to the rental car. It’s a good idea to have this insurance in case something unexpected happens while you’re driving. There are a couple of different ways to get rental car insurance, and it’s important to understand your options.

What Types of Rental Car Insurance are Available?

There are two main types of rental car insurance: collision damage waiver (CDW) and liability insurance.

CDW is an insurance policy that protects you from financial responsibility if you damage the rental car. This means you won’t have to pay for repairs or replacement if you get into an accident.

Liability insurance is a type of insurance that protects you from financial responsibility if you cause an accident that injures someone or damages their property. This is important because you could be held liable for significant medical bills or property damage costs if you are at fault for an accident.

Do You Need Rental Car Insurance?

You don’t always need to purchase rental car insurance. Your existing auto insurance policy may already provide some coverage. However, it’s important to check with your insurance company to make sure you’re covered. If you’re not covered by your own policy, you should definitely purchase rental car insurance.

How to Choose the Right Rental Car Insurance

When you’re choosing rental car insurance, it’s important to consider the following factors:

- The cost of the insurance

- The coverage provided

- Your existing auto insurance coverage

You should always shop around and compare prices from different rental car companies before you purchase insurance.

Comparing Collision vs. Liability Coverage

When you’re buying car insurance, you’ll come across a lot of different types of coverage. Two of the most common are collision and liability. These two types of coverage are important for different reasons, and it’s essential to understand the difference between them to ensure you have the right protection for your needs.

Collision Coverage

Collision coverage helps pay for repairs or replacement of your car if it’s damaged in an accident, regardless of who’s at fault. This coverage is optional in most states but is typically required if you have a car loan. Collision coverage will pay for repairs to your vehicle, minus your deductible.

For example, if you get into an accident with a deer and your car is totaled, collision coverage would pay for the cost of a new car, minus your deductible. If you’re at fault for the accident, your liability coverage would also pay for the other driver’s damages.

Liability Coverage

Liability coverage protects you financially if you cause an accident that injures someone or damages their property. It pays for the other person’s medical bills, lost wages, and property damage. This coverage is required by law in most states.

For example, if you cause an accident that results in another driver’s injuries, your liability coverage would pay for their medical bills and lost wages. Liability coverage also covers property damage, so if you hit another car, your liability coverage would pay for the repairs to their vehicle.

Which Coverage Do You Need?

Both collision and liability coverage are important, but which one you need depends on your individual circumstances. If you have a car loan, you’ll likely be required to carry collision coverage. However, if you have an older car with a low value, you may not need collision coverage since the cost of repairs may exceed the value of your car.

Liability coverage is essential for all drivers, regardless of the age or value of your car. It protects you financially if you cause an accident, so it’s crucial to have enough coverage to meet your state’s minimum requirements and potentially cover more significant claims.

Consult with Your Insurance Agent

It’s always best to consult with your insurance agent to determine which coverage is right for you. They can help you understand the different types of coverage available and create a policy that meets your specific needs and budget.

Deciding Between Primary and Secondary Coverage

When it comes to health insurance, you’ll often hear about primary and secondary coverage. These terms describe the order in which your insurance plans will pay for your medical expenses. Understanding the difference between primary and secondary coverage is crucial to ensuring you receive the most benefits from your insurance plans.

Primary Coverage

Primary coverage is the health insurance plan that is responsible for paying the majority of your medical expenses first. This is typically your main health insurance plan, whether it’s through your employer, an individual plan, or a government program like Medicare or Medicaid.

Secondary Coverage

Secondary coverage acts as a backup to your primary insurance. This plan usually kicks in after your primary coverage has paid its share of the costs. Secondary coverage is often provided by a spouse’s employer, a parent’s plan, or a supplemental insurance policy.

Why it Matters

The distinction between primary and secondary coverage is important because it determines how your medical bills are paid. When a healthcare provider bills for services, they will first submit the claim to your primary insurance. If your primary insurance pays a portion of the bill, the remaining amount will be sent to your secondary insurance for coverage.

Example

Let’s say you have health insurance through your employer (primary coverage) and your spouse has health insurance through their employer (secondary coverage). If you receive medical care, the bill will be submitted to your employer’s plan first. Once your employer’s plan has paid its share, your spouse’s plan will cover any remaining costs, up to its coverage limits.

Coordination of Benefits

The process of determining which insurance plan is primary and secondary is known as Coordination of Benefits (COB). COB rules vary depending on the insurance plans involved, so it’s important to check with both insurers to understand how their plans interact.

Key Points

- Primary coverage is your main health insurance plan.

- Secondary coverage acts as a backup to your primary coverage.

- Coordination of Benefits (COB) rules determine which plan is primary.

- Understanding the difference between primary and secondary coverage helps ensure you receive the most benefits from your insurance plans.

Knowing whether you have primary or secondary coverage is crucial for navigating your healthcare expenses. By understanding the difference and how COB rules apply to your plans, you can ensure you receive the maximum coverage and avoid unexpected out-of-pocket costs.

What is Personal Accident Insurance?

Personal accident insurance, also known as accident insurance, is a type of insurance that provides financial protection to policyholders in the event of an accident. It covers accidental death, disability, and medical expenses resulting from an unexpected and unforeseen event.

This type of insurance is designed to provide a safety net for individuals and their families in the case of an accident that could lead to significant financial hardship. It can help cover expenses such as lost wages, medical bills, and funeral costs.

Finding Insurance with Credit Card Benefits

Insurance can be expensive, and sometimes it can be difficult to find a policy that fits your needs and your budget. However, there are a few things you can do to get the most out of your insurance coverage. One option is to look for credit card benefits that can help you save money on your insurance premiums.

Some credit cards offer insurance benefits that can help you save money on your premiums. These benefits can include things like:

- Travel Insurance: This can help cover your expenses if you are sick or injured while traveling, or if your luggage is lost or stolen.

- Car Rental Insurance: This can help cover the cost of damage to a rental car.

- Purchase Protection: This can help protect you from damage or theft of items you purchase with your credit card.

- Extended Warranty: This can help extend the warranty on items you purchase with your credit card.

It’s important to note that not all credit cards offer these benefits, and the benefits offered by different credit cards can vary. So, it’s important to carefully compare different cards before you apply for one.

Here are a few tips for finding insurance with credit card benefits:

- Check with your current credit card issuer: Many credit card issuers offer insurance benefits, but you may not know about them unless you ask. Contact your issuer to find out what benefits are available to you.

- Compare different credit cards: You can compare credit cards from different issuers online or by visiting a credit card comparison website.

- Read the fine print: Be sure to read the terms and conditions of any credit card you apply for to understand the specific benefits offered and the limitations.

By following these tips, you can find a credit card that offers insurance benefits that can help you save money on your insurance premiums.

Checking for Coverage Limits

When you’re considering purchasing insurance, one of the most important things to consider is the coverage limits. These limits determine the maximum amount of money that the insurer will pay out for a covered claim. It’s crucial to understand these limits to ensure that you have adequate protection in the event of a loss.

Understanding Coverage Limits

Coverage limits are typically expressed as a dollar amount or a range of dollar amounts. For example, a homeowner’s insurance policy might have a coverage limit of $500,000 for dwelling coverage, $100,000 for personal property coverage, and $100,000 for liability coverage. These limits represent the maximum amount the insurer will pay out for each type of coverage.

How to Check Coverage Limits

You can typically find your coverage limits in your insurance policy. It’s important to review your policy carefully to understand the limits for each type of coverage. You can also contact your insurance agent or broker to discuss your coverage limits and ask any questions you may have.

Why Coverage Limits are Important

Coverage limits are important for several reasons:

- Protection against Financial Loss: Coverage limits help to protect you from significant financial losses if you experience a covered event.

- Peace of Mind: Knowing that you have adequate coverage limits can provide peace of mind, knowing that you’re protected in case of a loss.

- Avoiding Gaps in Coverage: If your coverage limits are too low, you may have gaps in coverage, meaning you might not be fully protected in the event of a major loss.

Adjusting Coverage Limits

You may need to adjust your coverage limits over time, as your circumstances change. For example, if you purchase a new home, you may need to increase your coverage limits to reflect the increased value of the property. If you acquire valuable possessions, you might need to increase your personal property coverage limits.

Checking for coverage limits is an essential step in the insurance process. It helps to ensure that you have adequate protection and peace of mind. By understanding your coverage limits and adjusting them as needed, you can avoid costly gaps in coverage and protect yourself financially.

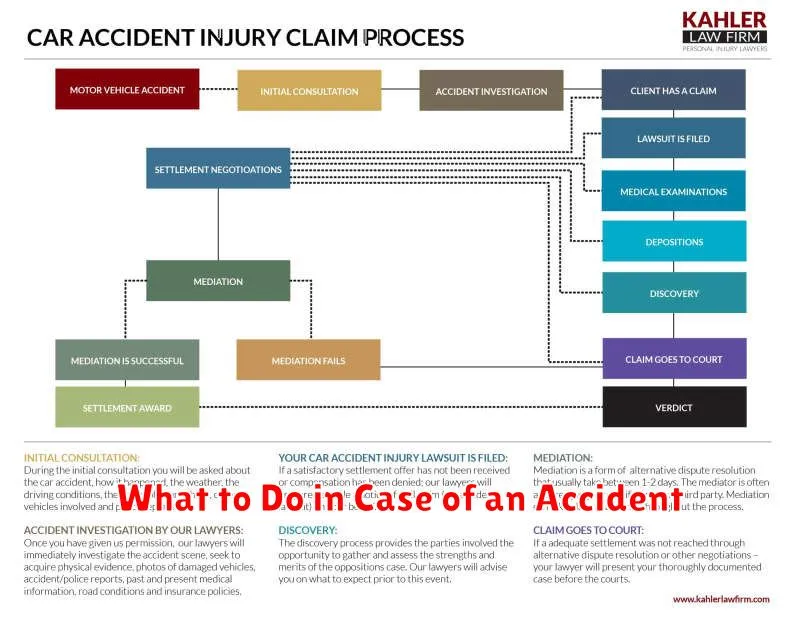

What to Do in Case of an Accident

Accidents can happen at any time, and it’s important to be prepared. Here are some steps you can take in case of an accident:

1. Ensure Safety: The first priority is to ensure the safety of yourself and anyone else involved. If the accident involves a vehicle, move the vehicle to a safe location if possible, or turn on your hazard lights. If there are injuries, call for emergency medical help immediately.

2. Assess the Situation: Once the scene is safe, assess the damage and determine what happened. Take note of any witnesses and their contact information.

3. Call the Authorities: If there are injuries or significant property damage, call the police and report the accident. You may also need to contact your insurance company.

4. Exchange Information: If there are other parties involved, exchange your contact information, driver’s license details, and insurance information.

5. Document the Accident: Take pictures of the damage, the scene of the accident, and any injuries. If possible, sketch a diagram of the accident, including the positions of vehicles and any relevant details.

6. Seek Medical Attention: If you have been injured, seek medical attention immediately. Even if you don’t feel injured at the time, it’s important to be checked by a medical professional to rule out any potential complications.

7. Report the Accident: Report the accident to your insurance company as soon as possible. Be sure to provide them with all of the necessary information, including the details of the accident, the names of the involved parties, and the contact information of witnesses.

8. Follow Up with Your Insurance Company: Your insurance company will handle the claims process, and you may need to provide additional information or documents. Follow up with them regularly to ensure that your claim is being processed properly.

9. Keep a Record: Maintain a record of all communication with the other parties involved, the police, and your insurance company. This documentation will be helpful if any legal issues arise.

10. Get Legal Advice: If you have any questions or concerns about your legal rights, or if the other party is disputing the details of the accident, it’s advisable to seek legal advice from an experienced attorney.

Tips for Filing Insurance Claims

Filing an insurance claim can be a daunting task, especially if you’ve never done it before. But it doesn’t have to be stressful. By following these tips, you can ensure a smooth and efficient claims process.

1. Report the Claim Promptly

The first step is to report your claim as soon as possible. This will help to preserve evidence and ensure that you meet any deadlines for filing a claim. Contact your insurance company directly, either by phone, email, or through their online portal.

2. Gather Necessary Documentation

To file your claim, you will need to provide certain documentation. This may include the following:

- Your insurance policy information

- Details about the incident, including date, time, and location

- Police report, if applicable

- Photographs or videos of the damage

- Estimates from repair professionals

3. Be Honest and Accurate

It’s important to be honest and accurate when providing information to your insurance company. Any inaccuracies or omissions could result in your claim being denied or delayed.

4. Follow Up Regularly

After filing your claim, be sure to follow up with your insurance company regularly to check on its progress. This will help you stay informed and ensure that your claim is moving forward efficiently.

5. Know Your Policy

Before you file a claim, it’s important to review your insurance policy and understand your coverage. This will help you determine if the claim is covered and what your responsibilities are.

6. Seek Professional Advice

If you’re unsure about any aspect of the claims process, don’t hesitate to seek professional advice. An insurance agent or attorney can help you understand your rights and responsibilities and ensure that your claim is handled fairly.

By following these tips, you can streamline the process of filing an insurance claim and maximize your chances of receiving a fair and prompt settlement.

Returning the Car without Extra Charges

Returning a rental car without any extra charges can be a smooth process if you follow the rental agreement and take some precautions. Here’s a guide to help you avoid any unexpected fees:

Understand the Rental Agreement

Before you even pick up the car, carefully read through the rental agreement. Pay attention to the following:

- Return date and time: Ensure you understand the exact time you need to return the car. Late fees can be significant.

- Fuel policy: Determine if you need to return the car with a full tank. Some companies offer a “full-to-full” policy, while others require you to return it with a certain amount of fuel.

- Additional fees: Look for any potential fees for things like late returns, tolls, cleaning, or damage.

Inspect the Car

Before driving off, thoroughly inspect the car for any existing damage. Take photos and note any scratches, dents, or other imperfections in the rental agreement. This will help you avoid being blamed for pre-existing damage.

Fuel Up

If you’re returning the car with a full-to-full policy, ensure you refuel it before returning it. You can usually find gas stations near the return location.

Clean the Interior

While not always mandatory, it’s a good practice to clean the interior of the car before returning it. This includes wiping down the seats, dashboard, and floor mats. A clean car makes a good impression.

Return on Time

Make sure you return the car on time to avoid late fees. If you anticipate a delay, contact the rental company immediately to inform them and arrange an extension if possible.

Check for Damage

After returning the car, do a final inspection with the rental company representative. Ensure they document any new damage and that it matches your initial report.

Review Your Bill

Once you’ve returned the car, carefully review your final bill. Ensure there are no unexpected charges. If you notice any errors, contact the rental company immediately to resolve the issue.

Tips for Avoiding Additional Charges

- Avoid driving on unpaved roads, as this could result in damage to the car.

- Be mindful of parking fees and tolls. Make sure you pay them on time.

- Consider purchasing additional insurance for added protection.

By following these guidelines, you can increase your chances of returning the rental car without any extra charges and enjoy a smooth and hassle-free experience.

{kind=link}